The ground segment market will reach a cumulative value of $80bn by 2032, according to the report titled Ground Segment Market Prospects from Euroconsult.

The ground segment market will reach a cumulative value of $80bn by 2032, according to the report titled Ground Segment Market Prospects from Euroconsult.

The report reveals promising trends in the ground segment market from 2023 to 2032. However, the situation is concentrated, regarding the considered market segments.

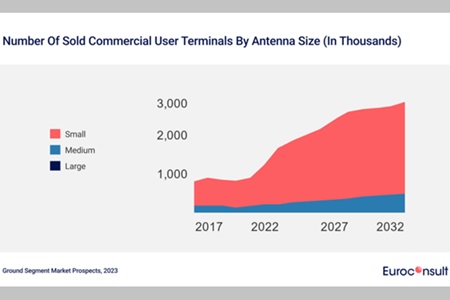

Euroconsult’s market intelligence predicts that non-geostationary (NGSO) constellation deployments will be a primary catalyst, leading to an increase by a 2.3 factor in the number of commercial user terminals by 2032, translating to an impressive 8.7% Compound Annual Growth Rate (CAGR). Flat Panel Antennas (FPA) also represent a massive growth area and will account for 74% of the sold commercial user terminals by 2032 compared to about 45% in 2022. The report highlights how the commercial user terminal market is benefitting from robust growth across various verticals. This expansion ranges from achieving universal broadband access to catering to the needs of mobility industries, enterprises, and government clients. Market demand is encouraging the development of terminals that seamlessly switch between low Earth orbit (LEO), medium Earth orbit (MEO) and geostationary orbit (GEO), enhancing performance and resiliency

Providers offering satellite-to-ground communication services, such as GSaaS, are enabling satellite operators to shift ground segment costs from capital expenditure (CAPEX) to operational expenditure (OPEX), mainly driven by Earth observation (EO) requirements. It’s particularly relevant for new operators testing their business models and aiming for progressive scaling. The Ground Station as a Service (GSaaS) market grew at an 11% CAGR during the last five years and is expected to continue expanding to reach $400m by 2027.

Jean Benoit Laithier, Principal Advisor at Euroconsult, said: “The dynamic evolution of the space segment, with flexible payloads and constellations, underscores the need for adaptable ground infrastructure to support advanced communication needs. The development of software-defined solutions at both space and ground levels will remain a major driver for ground segment manufacturers. These solutions encompass virtual functions that optimize capacity utilization, reduce costs and enhance overall efficiency, including software-defined networking, virtualisation and cloud technologies.”

At the ground station level, specific trends are emerging in different segments. Across the commercial sector, robust investments in High-Throughput Satellite (HTS) and Very High-Throughput Satellite (VHTS) systems, particularly in NGSO constellations, are driving growth in the data and services market. In contrast, the broadcast market is experiencing a decline, influenced by changing consumer behaviour and terrestrial competition. A renewed focus on defence satellite systems is also shaping the ground segment market. Modernisation cycles are being propelled by the launch of new satellite systems, with the US set to introduce new space assets and satellite systems, and several other countries in Europe and Asia following suit. As the increase in data & services market and defence does not counterbalance the decrease in broadcast, the number of sold ground stations should remain quite stable over the 2023 – 2032 period and reach 1,700 units in 2032.

Add Comment