Despite a slight slowdown, 1,155 satellites that are over 500 kg are expected to be ordered, with 1,285 to be launched, in the next decade, according to NSR’s Satellite Manufacturing and Launch Services, 9th Edition report.

Despite a slight slowdown, 1,155 satellites that are over 500 kg are expected to be ordered, with 1,285 to be launched, in the next decade, according to NSR’s Satellite Manufacturing and Launch Services, 9th Edition report.

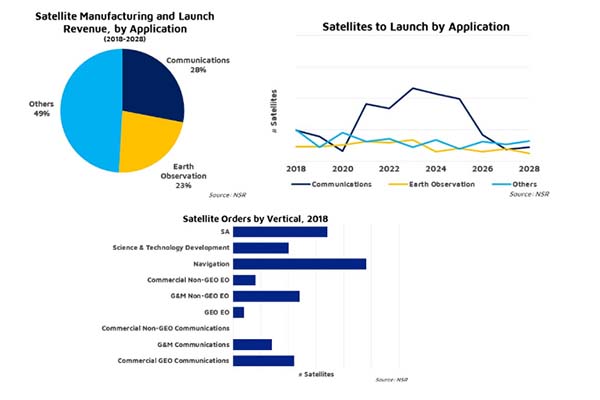

Between end of life replacement demand from most G&M heavy applications, such as Situational Awareness, and new demand from Science and Communications applications, the market for satellite launch and manufacturing is expected to grow robustly over the next decade.

Both GEO and Non-GEO markets will remain stable. The latter is expected to dominate, with over US $140bn in cumulative manufacturing and launch revenues. Government/ Military satellites will dominate the overall non-GEO market, as most commercial non-GEO systems are <500 kg. The GEO commercial market will experience a steady transition, as manufacturers and launch service providers try to creatively address the tailored requirements of operators.

“GEO communication satellite orders have been on a decline over the last few years, as the operators remain unclear about their future,” commented Shagun Sachdeva, NSR Senior Analyst and report co-author. “While the market is unlikely to reach the heady years of 18-20 annual Commercial GEO orders; increase in manufacturing efficiencies, availability of software defined small GEO satellites, and highly competitive launch prices are opening up new opportunities. GEO Commercial satcom satellite demand is expected to stabilize at an average of 13-15 satellite orders annually,” Sachdeva added.

Launch providers, like manufacturers, are re-examining their internal processes to cut costs and remain competitive in the market. “We are seeing established launch players phasing out their veteran launch vehicles in an effort to replace with upgraded versions, as well as over 100+ new launch actor hopefuls vying to enter the market worldwide, all looking for an edge by offering flexible and innovative solutions to their customers,” noted Leena Pivovarova, NSR Analyst and report co-author. “From reusability, to launches from a sea platform, to a blend of dedicated and rideshare offerings – launch service providers are considering different ways to lower the internal costs and offer better services to the customers. Cumulative revenues of $63B are expected from launch markets over the next decade,” Pivovarova added.

As the uncertainty in the market continues with declining capacity prices and the future of LEO satellite constellations, the industry will experience a key time of transition on a global scale. While the market is unlikely to return to traditionally accepted norms, new opportunities have begun to emerge for industry actors to grasp. Competitive pricing will be important to win more orders as operators continue to remain cautious of CAPEX spending, with internal cost reduction being essential for the survival of both the manufacturers and launch providers.

Add Comment