Global satellite capacity supply has surged eightfold over the past three years, reaching 27 Tbps in 2023, with Starlink accounting for more than 80% of this figure, according to the latest edition of the Satellite Connectivity & Video Market report by Novaspace.

Global satellite capacity supply has surged eightfold over the past three years, reaching 27 Tbps in 2023, with Starlink accounting for more than 80% of this figure, according to the latest edition of the Satellite Connectivity & Video Market report by Novaspace.

Delays in other constellation projects have contributed to Starlink’s dominance, but upcoming Low Earth Orbit (LEO) constellations, such as Telesat Lightspeed and Amazon Kuiper, alongside second-generation Starlink and Eutelsat OneWeb constellations, are expected to push capacity to 260 Tbps by 2029.

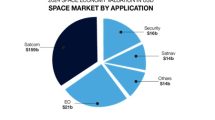

The rise of Non-Geostationary Satellite Orbit (NGSO) systems has reduced demand for Geostationary Earth Orbit (GEO) satellites as operators adopt a cautious “wait and see” strategy. Despite this, GEO systems represented about 85% of capacity revenues in 2023. However, NGSO capacity revenues are forecasted to grow at a 27% Compound Annual Growth Rate (CAGR), surpassing GEO by 2028 and reaching $18bn by 2033.

While GEO-High Throughput Satellite (GEO-HTS) systems continue to dominate premium sectors like aeronautical connectivity and military communications, Starlink captured 70% of total HTS traffic in 2023, intensifying competition in consumer broadband and maritime markets.

“Facing a shifting landscape marked by declining demand for video broadcasting, fluctuating mobility market patterns, and an influx of capacity from NGSO constellations, satcom operators have been exploring different strategies to survive,” said Dimitri Buchs, Manager at Novaspace and lead author of the Satellite Connectivity & Video Market report.

“In order to expand market reach, diversify service offerings, and enhance business resilience, capacity providers have been increasingly forming ‘multi-orbit’ partnerships. Market segments with lower price sensitivity, such as aero In-Flight Connectivity (IFC) and military communications are expected to drive the majority of demand for multi-orbit connectivity solutions. Overall, multi-orbit service revenues are anticipated to reach nearly $5bn by 2033.”

In response to rising competition, satellite operators are also pursuing both vertical and horizontal integration strategies. This includes two significant closed merger and acquisition deals in 2023 – Viasat’s acquisition of Inmarsat and Eutelsat’s merger with OneWeb – as well SES announcing it was acquiring Intelsat in 2024, with regulatory clearances expected to be received in 2025.

Consequently, the rising competition should contribute to the Average Revenue Per Unit (ARPU) for satellite capacity falling below $100 per Mbps per month across most segments by 2033. This price decline is set to unlock new opportunities in rural, remote, and under-connected areas, including those near urban centres and over oceans, driving global capacity demand to 73 Tbps by 2033 (27% CAGR).

The industry’s total service revenues are thus projected to reach approximately $117bn by 2033, capturing the expanding addressable market. However, the anticipated return to growth in service revenues may be delayed due to a continued rapid decline of the video segment in mature digital markets and a stagnation in previously growing emerging markets, such as South Asia. Additionally, delays in the deployment of NGSO constellations and VHTS capacity have also slowed service revenue growth in key data segments such as Enterprise Networks.

Add Comment